Information Disclosure based on TCFD Recommendations

Summary

In November 2020, our Group endorsed the TCFD (Task Force on Climate-related Financial Disclosures) recommendations and has been analyzing and disclosing information on the risks and opportunities that climate change presents to our business in accordance with four frameworks: "Governance," "Strategy," "Risk Management," and "Metrics and Targets." Moving forward, we will continue to deepen our analysis and promote the strengthening of our governance and business strategies regarding climate change response, while also taking into account disclosure requests both domestically and internationally.

Governance

For details on governance related to TCFD, please refer to the "Sustainability Promotion System" page.

Linking executive compensation and ESG indicators

Starting in fiscal 2022, our company has incorporated ESG indicators into the individual performance targets of executives. One of the ESG indicators we incorporate is climate change response, such as reducing CO2 emissions. By introducing incentives that link executive compensation and ESG indicators, we will strengthen executives' initiatives of climate change countermeasures and promote ESG Management.

Strategy

Prerequisites

The Group regards climate change as a very important management risk in terms of business continuity, and is analyzing risks and opportunities for below 2°C and 4°C scenarios.* In addition to climate change, we also regard the worsening of typhoon damage due to global warming as a risk factor.

*The below 2°C and 4°C scenarios are projections of how much the average temperature will rise from before the Industrial Revolution to the end of the 21st century, as presented in the Sixth Assessment Report of the Intergovernmental Panel on Climate Change (IPCC), which provides scientific evidence for countermeasures to global warming and is influential in international negotiations. The scenario with the lowest temperature rise (SSP1-1.9 scenario) predicts a rise of approximately 1.4°C, while the scenario with the highest temperature rise (SSP5-8.5 scenario) predicts a rise of approximately 4.4°C.

●Less than 2℃ scenario

With the introduction of strict environmental regulations and high carbon taxes, the world will achieve carbon neutrality by 2050. While the agricultural sector achieves net-zero CO2 emissions, procurement costs will increase due to growing demand for biofuels and stricter environmental regulations. As consumers become more environmentally conscious, demand for plant-based foods will expand.

The temperature in Japan has risen by approximately 1.4℃ compared to the end of the 20th century. Although the frequency and intensity of natural disasters (typhoons and floods) in Japan will increase, they will not worsen to the level assumed in the 4℃ scenario.

●4℃ scenario

Although progress is being made in reducing carbon emissions, carbon neutrality in 2050 will not be achieved. Natural disasters are becoming more severe and frequent, and the frequency of flood damage at suppliers and our own production bases is increasing. Due to rising temperatures, the yield and quality of agricultural crops are becoming worse.

Temperatures in Japan are expected to rise by approximately 2.3 degrees Celsius by around 2050 compared to the end of the 20th century. Additionally, as the frequency of typhoons increases, their intensity also increases. Flood frequency will be approximately 2 to 4 times more frequent than at the end of the 20th century.

| Target period | From now to 2050 |

|---|---|

| Target range | All businesses of J-Oil Mills Group |

Major: Potential impact on business performance (over 10 billion yen)

Medium: Potentially a significant impact on business performance (1 billion yen to less than 10 billion yen)

Small: Small impact on business performance (less than 1 billion yen)

High: Within 1 year Medium: Within 5 years Low: More than 5 years

Scenario: 2℃/1.5℃ Item: Transition risk

| Category |

Main risks | Risk Description | Impact | Urgency |

Existing initiatives | Response direction (goal) |

|---|---|---|---|---|---|---|

policy |

|

|

2.3 billion yen/year (*1) | Medium |

|

|

|

Medium | Medium | ||||

market |

|

|

Medium | Medium |

|

|

reputation |

|

|

Medium | Medium |

|

|

Scenario: 4°C Item: Physical risk

| Category |

Main risks | Risk Description | Impact | Urgency |

Existing initiatives | Response direction (goal) |

|---|---|---|---|---|---|---|

acute |

|

|

400 million yen/year (※4) | High |

|

|

|

Medium |

|

||||

Chronic |

|

|

High | Medium |

|

|

*1 IEA: International Energy Agency's forecast of emissions trading prices for developed countries in the NZE scenario (Net Zero Emissions by 2050 scenario) (2030): Calculated by multiplying 140 US$/t by the amount of emissions in fiscal 2024 and the average exchange rate for that period. The amount of risk decreased slightly from fiscal 2023 to fiscal 2024.

*2 PBF: Plant-based food

*3 Damage amounts were calculated based on risk assessments using Aqueduct, a global water risk assessment tool published by the World Resources Institute (WRI), and converted to annual damage amounts.

*4 BCP (Business Continuity Planning): Business continuity plan

*5 Main ingredients: soybean, canola

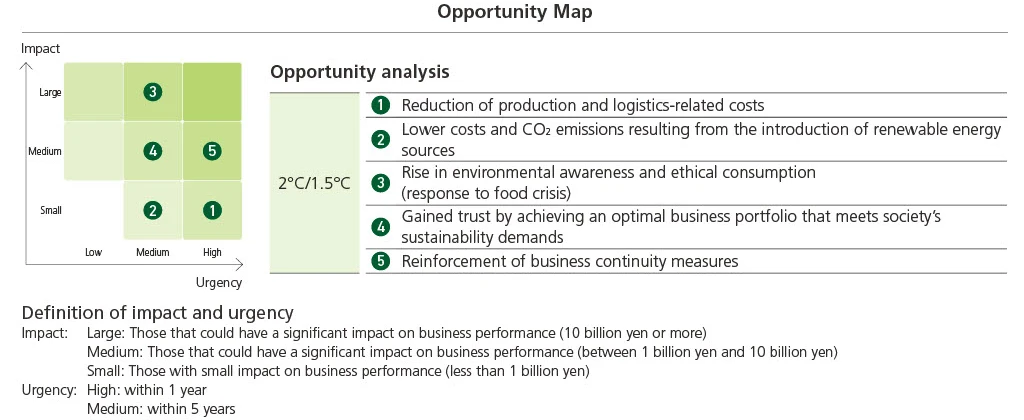

Scenario: 2°C/1.5°C

| Category |

Main Opportunities | Opportunity Description | Shadow sound Every time |

Urgency |

Existing initiatives | Response direction (goal) |

|---|---|---|---|---|---|---|

Resource Efficiency |

|

|

small | High |

|

|

Energy Source |

|

|

small | Medium |

|

|

market |

|

|

High | Medium |

|

|

Resilience |

|

|

Medium | Medium |

|

|

|

|

Medium | High |

|

|

*6 SAF: Sustainable Aviation Fuel

Additionally, we reviewed our materiality in 2021 and identified "Mitigation and adaptation to climate change" as one of our priority issues. In 2023, we reviewed our materiality again.

Please see below for the process of identifying materiality and determining relative importance.

Risk management

The Group has established a Risk Management Committee, chaired by the President and Member of the Board, which reports twice a year to the Board of Directors and the Executive Committee. Risk Management Committee manages significant company-wide risks, including climate change, from a short- to medium-term perspective and strives to prevent and avoid them. Sustainability Committee and the TCFD Subcommittee manage the risks and opportunities posed by climate change to our business from a medium- to long-term perspective under the Sustainability Promotion Structure. Based on the results of scenario analysis, we conduct a quantitative assessment of the financial impact of identified risks and opportunities and review countermeasures annually. The TCFD Subcommittee reports the results of discussions to Board of Directors and Executive Committee quarterly. Board of Directors provides necessary instructions or advice and monitors the situation. We will continue to expand and deepen the scope of our analysis, minimize risks, maximize opportunities, and strengthen resilience.

For details on risk management related to sustainability in general, please refer to the "Risk Management" page.

Metrics and goals

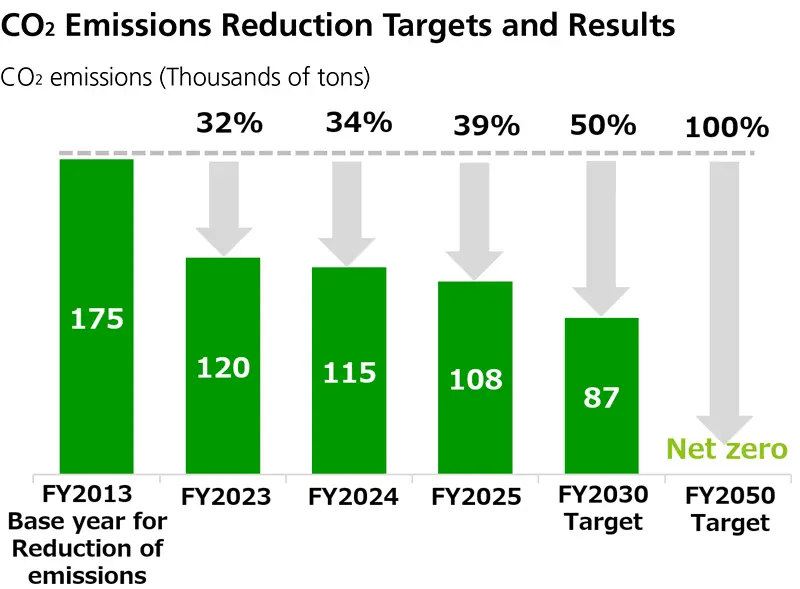

We aim to reduce CO2 emissions by 50% by FY2030 compared to FY2013 levels (Scope 1 and 2) and achieve carbon neutrality by FY2050. We also aim to reduce emissions across the entire supply chain (Scope 3) by collaborating with suppliers on CO2 emissions related to the raw materials we purchase and the manufacturing of our products. For categories 1 and 4, which have high emissions, we will improve the accuracy of our calculations, set reduction targets, and consider reduction methods by obtaining emission information from producing country organizations regarding the production stages of our main raw materials, soybean and canola. In addition, we will utilize Internal Carbon Pricing (ICP), which was introduced in April 2023, to promote investment and investment decision-making toward CO2 emission reduction.

Main initiatives

- Reduction of energy consumption (process optimization, energy saving, introduction of high-efficiency equipment, etc.)

- Utilization of renewable energy (use of biomass fuel, etc.)